I have repeatedly suggested that investors own “real assets” so it’s probably worth taking a look at just what that means and why we believe investors should own these assets in their portfolios. Real assets are physical assets that have an intrinsic worth due to their substance and physical properties, but tend to be less liquid. They provide good portfolio diversification since they often move in opposite directions to financial assets like stocks and bonds. Examples include real estate, farmland, infrastructure and commodities. Financial assets derive their value based on a contractual right or ownership claim and offer better liquidity. Examples include stocks, bonds, cash, etc.

In past notes I made the argument that stocks and bonds have had the benefit of almost 40 years of declining interest rates, the impact of globalization, and the boomer generation that entered the workforce then putting their savings into financial assets. That tailwind is set to become a headwind in the years ahead, making it more difficult to generate performance. Ever since the financial crisis, central banks have taken it upon themselves to provide the liquidity needed to ensure these asset prices continue their upward trajectory and since the outbreak of the global pandemic, they’ve conjured up trillions of dollars more of new money.

The chart above shows how the price earnings multiple has spiked higher during this period of unprecedented expansion in the Federal Reserve balance sheet. The additional $3 trillion added by the Fed has helped push markets higher as a result. The higher prices investors are paying for stocks, is happening without any increase in underlying earnings (in fact, they’re likely to be much lower). Paying a higher price for the same thing (or maybe less) is called inflation, but strangely, nobody ever calls it that when it happens with stocks and bonds. Since the sell-off bottomed out in late March, we have seen the greatest 50-day return in equities. It might be worth noting that in our world, we haven’t seen any impact on the prices of farms we are looking to acquire. That easy money hasn’t made it into the real economy, yet.

I presented the chart below in a previous note but it also makes the point about financial assets relative to real assets. With interest rates at historical lows and U.S. equity market valuations near all-time highs (market cap relative to GDP), it shouldn’t surprise that the ratio of commodities to the S&P 500 is at a multi-decade low (all-time low?). Historically, these levels have marked turning points and investors should probably be leery of such extremes.

The turning point happens when we get to extreme levels and can happen either through a material correction in financial assets, a spike in inflation, or both. I don’t know what happens next, but it seems like folly to assume it continues this way for years to come. It also seems foolish to assume that if central banks really want inflation that they cannot print enough money to eventually accomplish that. And you should probably ask yourself, how else besides inflation will these debt levels ever be dealt with?

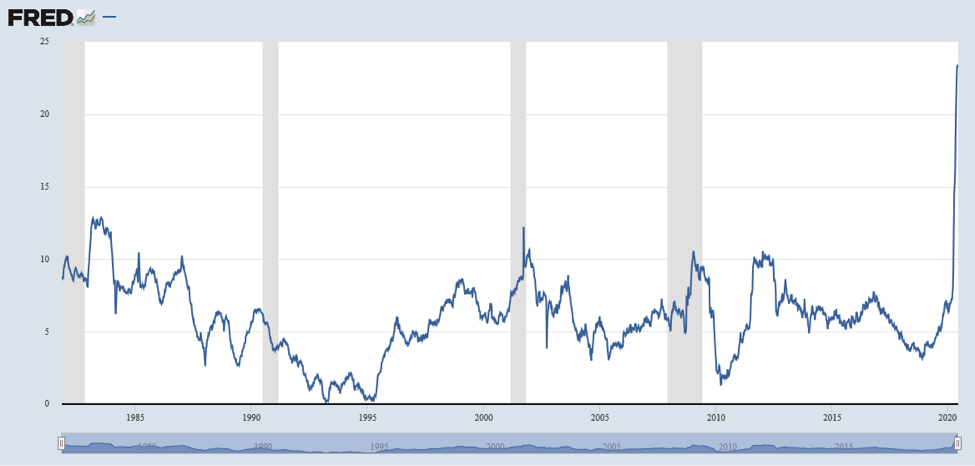

In the meantime, a look at the U.S. response to the pandemic shows the fastest increase in M2 money supply in 40 years. This number will probably look even worse in the months to come as the U.S. contemplates more stimulus measures heading into an election. It’s worth noting that similar measures are being taken by every developed country’s central bank.

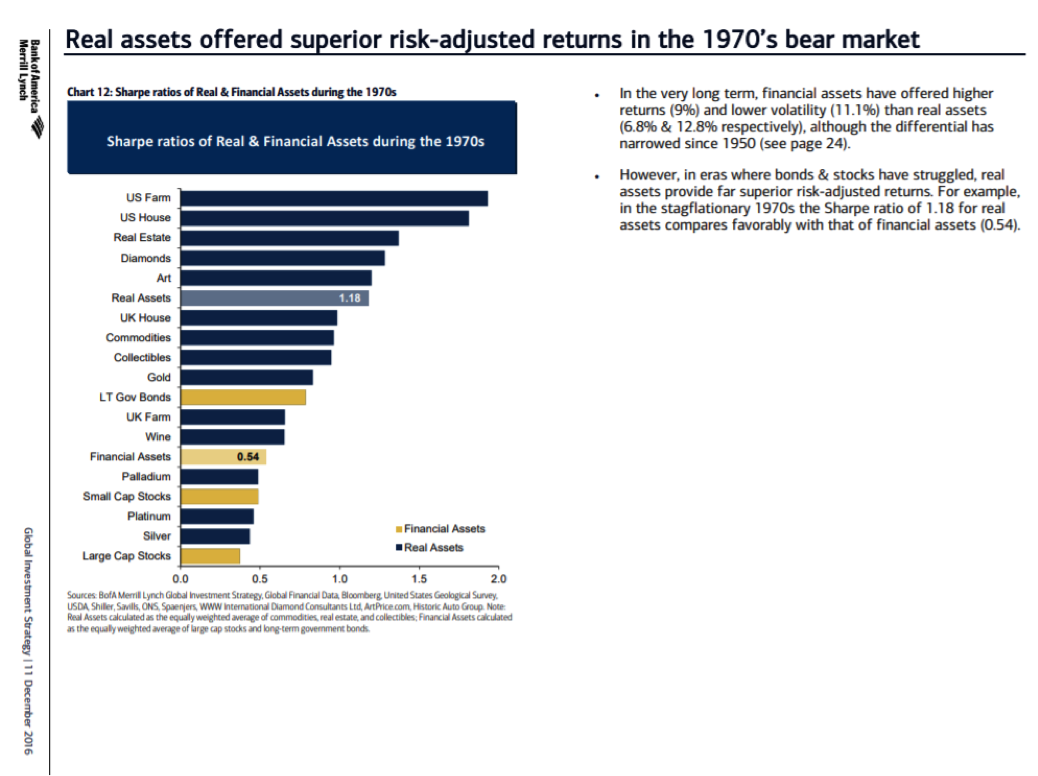

Below is a chart from a report written by Michael Hartnett, the Chief Investment Strategist for Bank of America Merrill Lynch that served as a primer for real assets. The chart shows that during the bear market of the 1970s when inflation was high, financial assets underperformed and real assets outperformed. It also shows that during that period, farmland was the best performing asset.

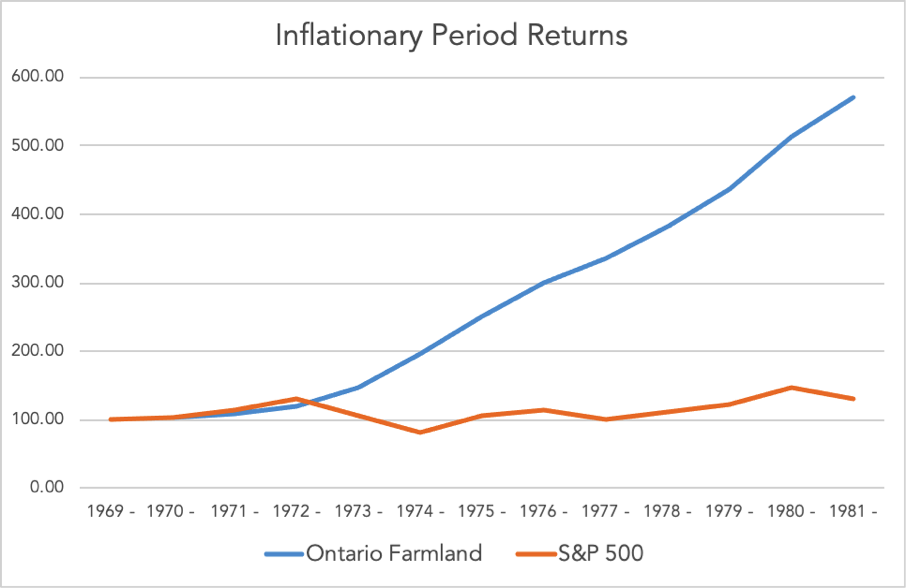

Using data from Statistics Canada, I was able to generate a graph comparing returns between a broad index like the S&P 500 with Ontario farmland. The chart supports the observation by the Chief Strategist at Merrill Lynch.

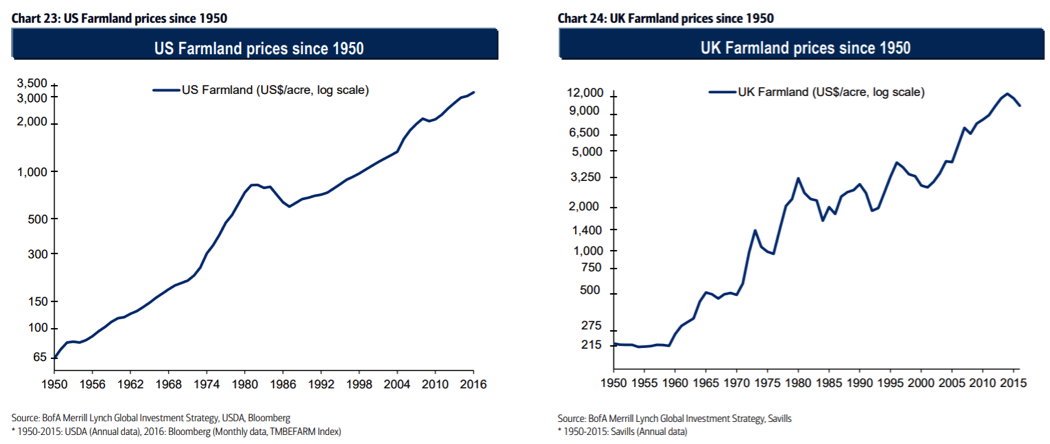

Our chart supports the view that farmland is a good hedge against periods of elevated inflation, but the reality is that farmland around the world has generally provided good returns for more than half a century. Farmland isn’t just an asset you hold to protect your portfolio from inflationary periods. I’ve said this before but the advances in technology, innovation in mechanical equipment and breakthroughs in the biology of crops have meant that the yields and efficiencies of farms have been improving during this period. The chart below, also from the Bank of America report, shows the appreciation in farmland has been reflecting those improvements for years.

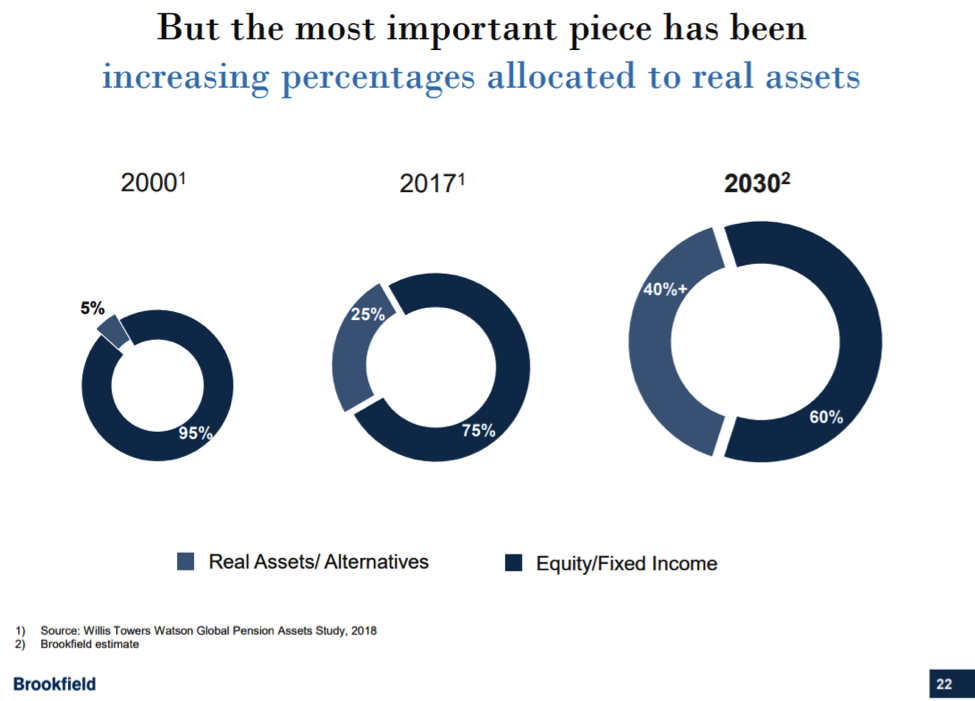

In a recent shareholder document, Brookfield included some estimates on what they expect the allocation to real assets to be in the years ahead.

Most investors have been lulled into a sense of complacency about the prices of financial assets. But it’s worth remembering that operations by central banks, whereby they print money to buy stocks (Bank of Japan and Swiss National Bank) and bonds (almost every central bank in the developed world) mean there isn’t true price discovery in financial assets. Creating money out of thin air to use to purchase assets, often with the stated goal to push prices higher (wealth effect), has created some distortions. This is most evident in bond markets, where the buying has been greatest in order to keep rates down. The yield on most developed countries’ government bonds are below 100 bps (just over 50 bps here in Canada), which means if you are holding on to these bonds, you need rates to go even lower (negative?) in order to realize much of a return (capital gain). The governments that issue these bonds are running higher deficits so their central banks have resorted to printing money to help pay for all of the bond issuance. This means the units (currency) in which these bonds are denominated are being debased while investors collect only a few basis points.

Time to Reconsider the Asset Mix

Remember the chart above from the Brookfield report? Well, if you are running a large portfolio that seeks to match assets with its long dated liabilities (pension or insurance funds), it might make sense to reconsider those government bond holdings and replace them with an asset like farmland. The yield on farmland in most cases is greater than that on government bonds, but unlike the debasing happening in currencies (the units in which the bonds are denominated), you own an asset where the production yield has been increasing for over half a century with the help of technology and innovation. That means that rather than having your investment’s value debased by money printing operations, the underlying asset you own is likely to generate more physical yield over time. Also, you should probably ask yourself “is there any other way out of the global debt bubble than to try and inflate it away”? If governments continue to debase their currencies, they will eventually achieve the inflation they so desperately want. When that happens, owning a long dated bond yielding 50 bps is probably the last thing you want to own. An inflationary environment would eventually force central banks to push rates higher. That will make owning a long dated bond with almost zero yield seem like a really bad idea and a tough thing to explain to stakeholders. Conversely, the last time we had an extended period of inflation, farmland dramatically outperformed financial assets (as per Merrill Lynch report and Statistics Canada figures). In the meantime, you own an asset that is growing production vs. one that is being debased AND paying a lower yield.

The shift in asset mix that Brookfield is forecasting towards more real assets is very likely to happen over the balance of this decade. The risk/return profile of owning bonds (and other financial assets) vs. an asset like farmland in this environment should mean that decision gets made sooner rather than later

Written by AGinvest Senior Vice President of Business Development, Anthony Faiella. To reach Anthony please email Anthony.Faiella@AGinvestCanada.com

This information does not constitute financial or other professional advice and is general in nature. It does not take into account your specific circumstances and should not be acted on without full understanding of your current situation and future goals and objectives by a fully qualified financial advisor.