……either way, history suggests owning farmland is a good bet

In my conversations with investors and potential investors since joining AGinvest, I’ve found there is a very distinct difference in how people from different backgrounds think about an investment in farmland. First of all, as someone who has only ever worked in the investment industry and spent almost all of that time in front of a screen with real-time pricing of investments, including stocks, bonds, commodities, etc., I can relate to the people in the investment industry. I understand their need to know the price of everything and quantify returns at every given moment. After all, they make their living by buying and selling investments, or as an agent on those transactions. But when I speak with investors that have built businesses, outside of the investment industry or finance, they have a very different perspective. They know about making “stuff” and building a business that can operate at a profit. They have created wealth by running their business efficiently, without needing to know the value of it every minute. The ones I’ve met with were too busy building their businesses to spend much time contemplating the value of their business each day. Then at some point, after years of running their business, they realized they had become very wealthy operating that business. They also understand the benefit of having an asset that is able to produce more over time, which is also an attribute of farmland.

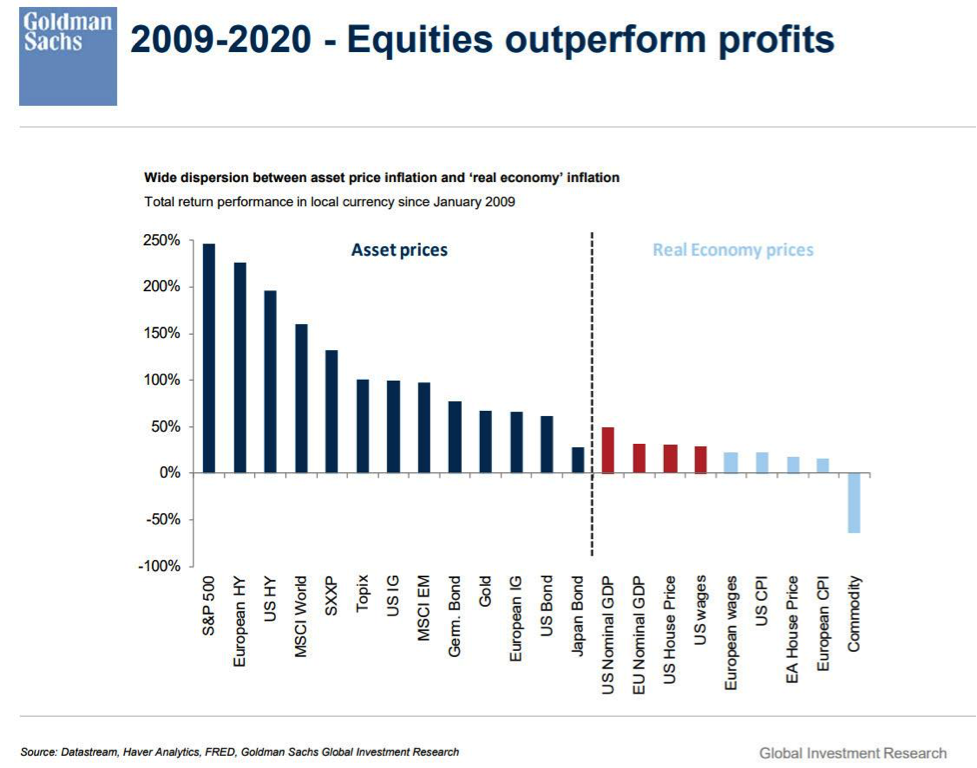

Despite all those years sitting in front of a quote screen, I can appreciate the true, tangible value being created by operators of businesses that can utilize assets effectively and create more value from assets. I also believe that we are heading for a period in time where you will need to own real assets that generate tangible wealth and returns. The response to previous recessions and the buildup of debt have left us with a world where financial assets and assets that are financed with debt, have achieved outsized returns relative to the real economy. Now we have global economies recording the sharpest declines since at least the Great Depression and the greatest monetary response in history. That response from governments and central banks has allowed financial assets to maintain values that seem increasingly detached from the underlying businesses and economy.

The monetary response to this crisis has also sparked a debate amongst forecasters as to whether it’s enough to avoid a deflationary fallout from the global shutdown or spark a period of high inflation. Nobody can say for certain how this will work out, but it does appear as though one outcome, or possibly both, is/are likely to result. Given that likelihood, and using the data from Statistics Canada, I went back to see how our investment fared in times of deflation and inflation. It turns out that during both periods (a decade of deflation, 1930’s and inflation, 1970’s), Ontario farmland outperformed the S&P 500 materially. There is no guarantee that it would happen again, but it seems to make sense that a productive asset would outperform a financial/paper asset during such periods. And based on where financial assets are currently trading and how they got there, history might just be poised to repeat.

How did we get here?

Since the outbreak of this global pandemic, the world’s central banks have taken to bailing out asset prices and buying up their government’s debt, being issued at record amounts to pay for their unprecedented support programs. Previous recessions were met with aggressive interest rate cuts and the financial crisis even included a bailout of the bad actors, which meant the debt was allowed to survive and grow. More than 10 years later, the result is a global debt bubble unlike any in history (the global debt-to-GDP hit an all-time high of over 322% in Q3 2019 – Link to report), and that was before current crisis even began. Rather than allow recessions to take their course and clear out the malinvestment, much like a brush fire, or “prescribed fire”, clears out the underbrush allowing a forest to grow healthier, the world’s central bankers decided they know better and took actions to “save the economy”. Taking that analogy further, forest fires are a natural and necessary part of the ecosystem that clear out the underbrush, allowing sunlight to reach the forest floor and freeing plants from invasive weeds. Fires are followed by a growth spurt in the trees.

That analogy might be a good place to start when trying to understand why the recovery since the financial crisis has been the most muted in history. Recessions are supposed to have the same effect on an economy by clearing out the bad debt (debt on underproductive assets) allowing an economy to grow unimpaired by bad businesses supported by bad debt. Instead, not only did policies coming out of the financial crisis not allow for bad debt to default (disappear), they encouraged business models that didn’t even make money and allowed them to prosper. In fact, more than 80% of IPOs in 2018 and 70% of IPOs in 2019, had negative earnings. So accommodating (distorted) had capital markets become, that businesses with no earnings, and in some cases, no prospect of earnings, were coming public and garnering huge valuations. All of this capacity spawns deflation and mutes economic growth. And while the easy money fostered deflation in the economy, it was fueling inflation in asset prices (as we showed in our previous note), with valuation multiples increasing throughout the cycle. In other words, the inflation appeared only in the places were the capital and leverage was chasing after a finite asset (i.e. a stock market with an ever shrinking number of shares outstanding) and in assets that can be purchased with leverage.

The other impact from this approach, is that recessions are becoming sharper and more severe requiring ever increasing amounts for bailouts, and this one is requiring trillions in new money to keep it going. Now before you respond that this is all because of the global pandemic, it’s worth remembering that both the ECB and Federal Reserve began to ramp up their QE programs in the second half of 2019 (ECB increased theirs while the Fed began supporting the repo market with their “no QE”, QE program). Those actions were in response to cracks that had already begun to appear with slowdowns in economies that saw global trade sink to the lowest levels since the crisis and flair ups in the overnight lending market. I would also like to point out that the “greatest economy ever” was already in need of a $1 trillion deficit, roughly 5% of GDP to achieve growth of roughly half that amount in their GDP. Let that math sink in. This global debt bubble was eventually going to find a pin, but instead it found a grenade in the form of this global pandemic. Regardless of what caused it, any slowdown would have made many corporations vulnerable, given the balance sheet leverage (damage) they had incurred with buybacks or their unviable business models. All of that debt had created the equivalent of a lot of dry tinder on the forest floor.

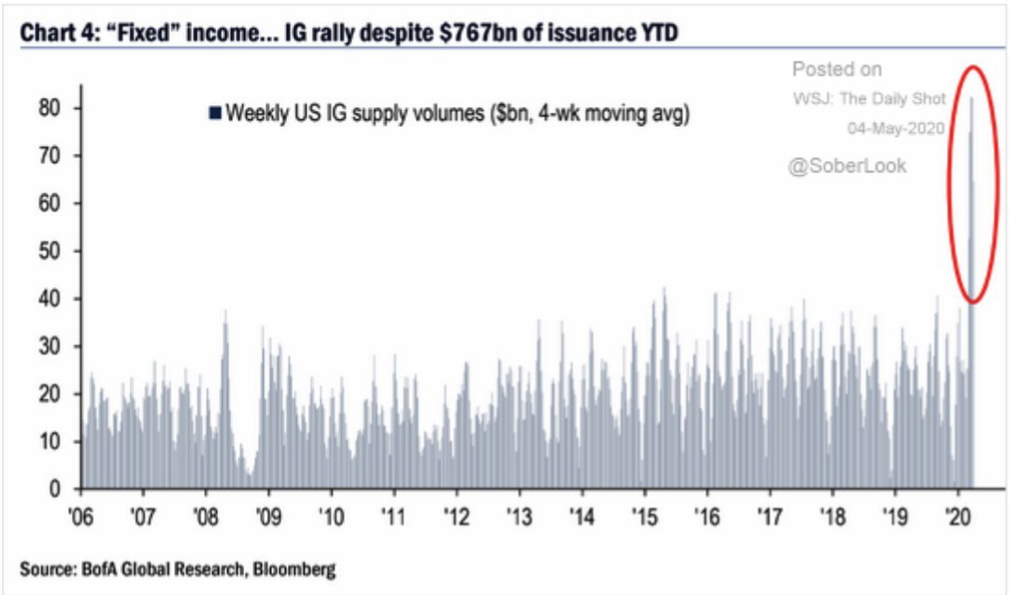

Anyway, that’s how we got here, so now we must deal with a global economy that has record debt levels and interest rates at the lowest levels, possibly in history. The U.S. Federal Reserve, keeper of the world’s reserve currency and de facto setter of global interest rates, recognizes that if a debt bubble bursts, you get a deflationary bust (i.e. U.S. economy post-1929 and Japan’s economy post-1989). So they’ve set out to bail out bond markets, since that’s where the debt gets refinanced. The Fed stepped in to buy U.S. Treasuries (they bought more Treasuries in the 6 weeks following the shutdown than the net increase in foreign holdings over the previous 6 years) and they’ve announced they intend to buy corporate bonds (which is technically illegal for them to do, but let’s not nitpick). Their implied support of the bond market has allowed corporate issuers of investment grade bonds to set issuance records for two straight months and allowed junk bond issuance of almost $32 billion in April, the highest level in three years (Link to source).

All of this debt issuance is happening during the worst global economic collapse since the depression…..so much for prescribed burns. Maybe when this is all over they should replace central bankers with forest rangers. They probably couldn’t do any worse than what’s been done to date…..just a thought.

The chart above should further confirm the disconnect between the financial economy and the real economy. With record levels of jobless claims and record drops in economic activity, investors would not be rushing to buy debt issuance without the backstop of the Federal Reserve and their intention to buy these securities.

The case for deflation

The solution to this crisis is the same as it always is for the central banks; provide more liquidity (when you have a hammer….). While the central banks can provide the liquidity, if spending levels are impaired going forward, this is likely to be about solvency and not liquidity. North American consumer debt levels are at all-time highs on both sides of the border, so it seems unlikely the consumer will continue to spend at the levels prior to the pandemic, given the job losses. If this turns out to be the end of the credit cycle, there is likely to be a deflationary period that ensues. This is the scenario many global strategists are predicting for what may lie ahead. The reality is that all of that credit creation over the past few decades, has effectively been money creation and much of it went towards pushing asset prices higher. Most of the money created through QE is being used by the Fed to buy government debt, displacing the natural buyer of that debt, forcing them out along the risk curve to buy corporate debt for the higher yield they require. Under the new program, the Fed announced they intend to also buy the debt of corporates. Injecting trillions into bond markets, ensures a bid for bonds that would otherwise be destroyed in a recession. In other words, much of that QE money is not making its way into the general economy, but instead is just going towards maintaining asset prices (swapping out otherwise bad debt for newly printed money) and supporting a government running huge deficits to keep the economy going. The proof is in the thousands lined up for hours in U.S. cities for a bag of food, despite more than $2.2 trillion in U.S. “bailouts”. Barely any of the $2.2 trillion actually went to Main Street and instead went to corporates and bailing out the system.

In setting rates so low for the entire cycle, the Federal Reserve was providing all of these businesses with almost unlimited access to capital. It also ensured we continued to have excess capacity throughout even the longest economic expansion in history. The problem is that as the world borrowed and lived beyond its means, global capacity was built to supply that level of spending and it was financed at the lowest interest rates ever. If spending levels drop, current capacity will need to be re-priced even lower, especially if businesses aren’t left to go bankrupt allowing capacity to be removed. If credit defaults, assets may need to be sold into an environment with less liquidity and lower prices will result.

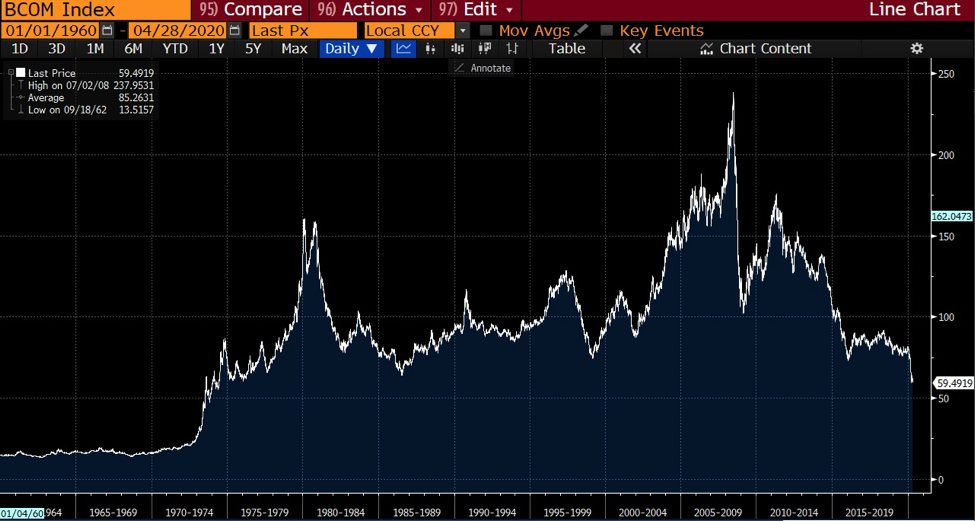

The signs of this deflationary fallout can already be seen in commodities. The Bloomberg Commodity Index, which includes 22 commodities, has returned to levels last seen in 1973. That drop is even worse when you consider that the U.S. dollar has been devalued materially since then. As measured in gold bullion, the U.S. dollar has lost more than 98% of its purchasing power since 1971. That should give you a sense of the magnitude of the drop in commodity prices in real terms. On its own, this is a good thing that allows commodities and the things they’re used to make, more accessible to the masses. It’s also a testament to human ingenuity and our ability to make things more efficiently and at a lower cost.

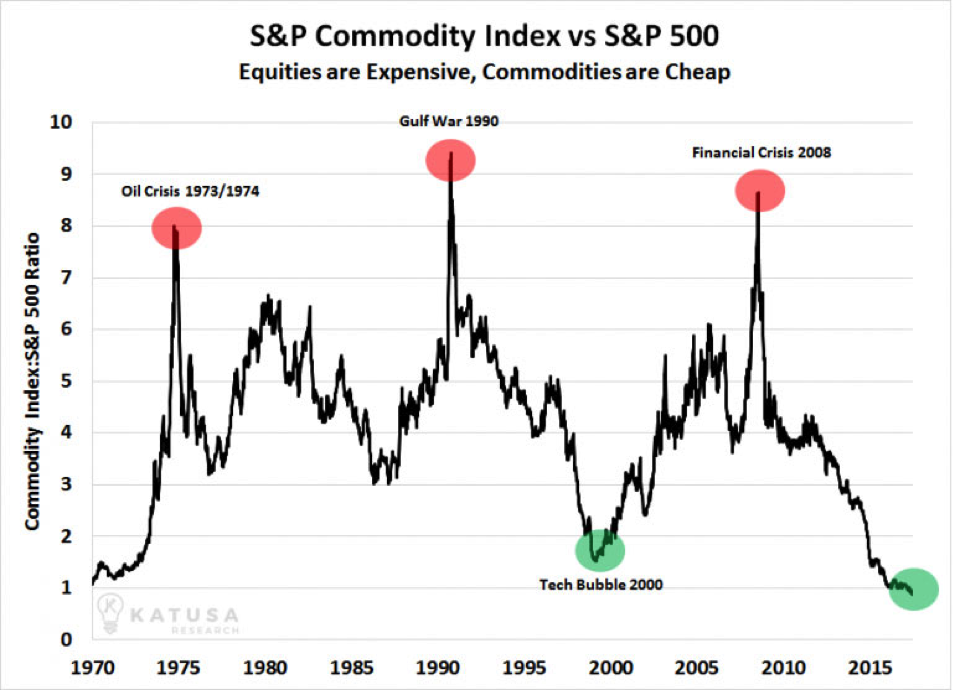

But the value of financial assets, which have been the beneficiary of that easy money and effectively the Fed’s target for creating a “wealth effect”, are the highest they’ve been as compared to commodities in at least 50 years.

The chart above reflects the extreme disconnect between the deflationary pressure that exists in the real economy and the inflation we’ve seen in financial assets. I believe Ray Dalio refers to it as the “Real Economy” and the “Financial Economy”. The Financial Economy has been inflated through the depreciation of the currencies while the Real Economy is reflecting the impact of the excess capacity and the deflationary impact of technology and innovation.

Those arguing for deflation may well be proven right in the short to intermediate term. Despite all of the unprecedented money printing we are seeing, much of it isn’t making it into the economy (e.g. mile-long food lines). So the excess capacity in a world where spending is likely to come down and savings rates are likely to go up, will mean deflation wins out….initially.

Inflation won’t likely be far behind

But if history has taught us anything, it’s that governments like to spend money and promise things they can’t afford. Once governments realize they can spend well beyond their means and just have their “independent” central banks buy up the debt, the spending will only go in one direction. There is no putting the genie back in the bottle. I suspect that handing out money to people and industries will become too easy, especially since it will happen during a time of deflation (won’t show up in inflation) and will seem necessary. It also means it won’t be long before Main Street begins to get their fair share of the conjured-up money. The wealth disparity that exists could quickly lead to populism if stock markets soar and food lines grow longer.

Back when the financial crisis hit, central banks around the world decided they needed to purchase assets (create money out of thin air to support asset prices). Ever since then, there has been at least one central bank continuing to provide more liquidity, and trillions have been printed. The global pandemic has resulted in another similar response, with virtually every central bank in the world capable of printing, doing so. This has helped bring equity markets back, resulted in record issuance of investment grade bonds over the past month, and brought the junk bond market to values just shy of where they were trading before the pandemic. This recovery in asset prices has been a result of the liquidity provided and the assurance that central banks will defend asset prices. If your portfolio is filled with only financial assets, you might want to consider the value of having a portfolio filled with investments that are reliant on conjured-up money in order to maintain their value. The chart above shows us that in the past, when we’ve reached extremes in valuation of financial assets (S&P 500) relative to commodities (inflation measure), a sharp bounce ensued that was caused by either a drop in prices of financial (paper) assets and/or a bounce in inflation.

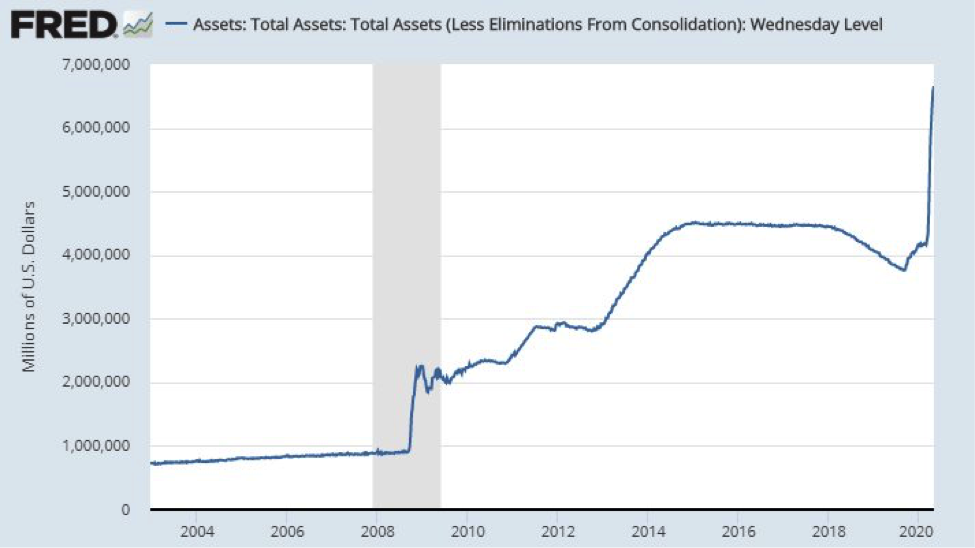

One quick look at the Federal Reserve’s balance sheet (money created out of thin air) should be used as a reference point explaining the strength in financial assets, especially since that money hasn’t shown up in other inflation drivers like commodities. What should also be apparent is that it requires more and more of this newly created money (not to mention the additional debt created) to keep asset prices higher.

Money has been printed for more than 10 years for the sole purpose of maintaining (raising?) asset prices. They call it the “wealth effect” and from the outset, central banks made no secret of their intention. Fundamentals and price discovery were long ago made irrelevant. The Federal Reserve raised interest rates four times in 2018 at the same time they were letting their balance sheet run off (Quantitative Tightening). That tightening in liquidity resulted in a violent sell-off by the end of that year. In order to stop that selloff, the Federal Reserve cried “uncle” and promised to be more accommodative. That announcement was followed by four rate cuts in 2019 and caused markets to rebound dramatically. At the end of the third quarter last year, the overnight lending market began to seize up with rates spiking higher. The solution required hundreds of billions in liquidity that they said was “not QE” (spoiler alert: it was conjured up money to buy assets in order to maintain the price, so….). That “solution” caused markets to once again race higher. In March of this year, as the global pandemic sent highly levered, expensive markets (both stock and bond) reeling, the Fed stepped in with trillions in liquidity, once again earmarked for asset purchases. Notice a trend here? Also, each successive bailout is requiring more and more money, and the price of many of these investments is becoming increasingly detached from the underlying economy and fundamentals.

According to Bank of America, year to date, we have already had $16.4 trillion in global policy stimulus; $9 trillion of QE and $7.4 trillion of fiscal stimulus. If we assume $90 trillion in global GDP (likely to be a very generous estimate given the hit to GDP around the world) then we already have the equivalent of almost 20% of global GDP in stimulus, and the year isn’t half over. The futures market has already begun to price in negative rates on U.S. Treasury securities (debt) and the U.S. government is talking about the need for grants, negative payroll taxes and more bailout programs. In Canada, our free spending government is bailing out everyone, giving raises to the essential workers and even renovating the prime minister’s cottage……no point wasting an opportunity to sneak in some extra spending. In other words, while it may take them some time to fight the deflation, central banks may well hit the necessary keystrokes and add enough digits to ignite the inflation they so desperately desire.

Let’s get to the point

I believe we will eventually wind up with a much higher inflationary environment. There are a number of factors that would suggest countries will try to repatriate industries meaning a reversal of the globalization trend that helped to lower inflation all these years. The logistics of social distancing and what it means for the efficiency of business will also help contribute to higher costs and fuel inflation. And of course, central bankers with itchy trigger fingers hitting their keyboards to create more and more money.

Either way, I thought it worth going back in history to see how different assets worked in previous similar environments.

A look at the period from 1930 – 1939 where inflation was negative (deflation) or relatively low for much of the decade, the returns were:

Ontario farmland CAGR -2.6%

S&P 500 CAGR -5.4%

Note: the comparison does not include either dividend yields or farm yields. It’s also worth noting that farm production yields were relatively flat during the 1930s and in fact, when I looked at corn yields per acre in the U..S over the past century, they actually declined during the 30s (difficult to find comparable Canadian data for the 30s). The big increases in farm yields began in the 1960s and have accelerated ever since.

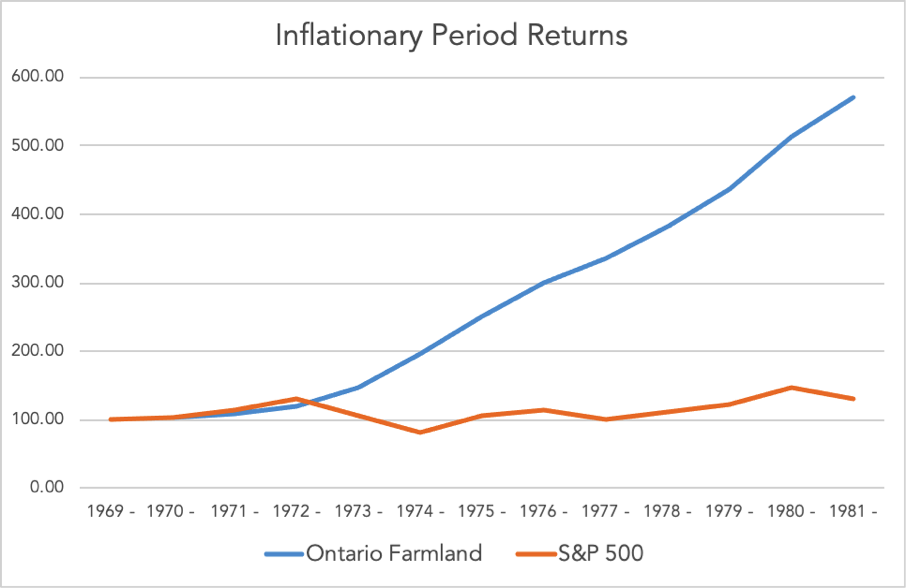

When looking at the period from 1970 – 1982, a period during which we regularly had mid-single digit or even double-digit inflation (that period included a recession which began in 1970 and another recession that began in 1980 and ended in 1982). Over that thirteen-year period of relatively high inflation, the returns were:

Ontario farmland CAGR: 13.9%

S&P 500 CAGR: 2%

Note: dividend and farm yields were not included in those calculations. They only reflect absolute levels.

I would draw your attention to the year 1971, when in August of that year, Nixon closed the gold window and money became unhinged. Removing the option of trading dollars for gold allowed them to print money. The decade that followed saw much higher inflation. But that inflation didn’t help the stock market, instead it drove gold and farmland prices higher. We are approaching, if not already knee-deep in it, another era of unhinged money. We’ve already seen the fastest rate of increase in M2 Money Supply since the WWII, and if history is any guide, it might be wise to own assets that allow you to maintain your wealth and its purchasing power.

It’s time to own some Real Economy assets in the portfolio

Printing money has never been easier (no printing press needed, just a keyboard!!!) and that printed money is primarily being used to support financial markets through direct buying of assets. It’s interesting that the commodities index is making multi-decade lows despite the greatest expansion in money supply since the Second World War while financial markets race higher in the face of an unprecedented economic global collapse. I believe it is shows the extent to which the financial economy is detached from the real economy. If that’s true, it might make sense to own assets that create and accrue value to their owner based on what they produce. It certainly appears the value resides in the “Real Economy”, especially relative to the “Financial Economy”. A recent Bloomberg article quoted Paul Tudor Jones as saying, “We are witnessing the Great Monetary Inflation – an unprecedented expansion of every form of money unlike anything the developed world has ever seen”. During the recent Berkshire Hathaway annual meeting, Warren Buffett was asked about the current monetary backdrop of money printing and negative rates. Buffett suggested, “You better own equities or you better own something…” except of course he was a seller of equities in the weeks preceding the meeting. Based on monetary actions seen during the two most recent crisis, debt defaults are not even on the table, meaning governments will most likely turn to printing and devaluing currency as the easiest way out of this debt bubble. So while we may not yet see signs of inflation in the general economy, it seems unwise to bet against it over the longer term. The last time we saw an extended period of inflation, financial assets (both stocks and bonds) did not fare well. During such periods, history suggests that wealth is better protected with real assets generating real returns; just ask anyone who’s built a business.

Written by AGinvest Senior Vice President of Business Development, Anthony Faiella. To reach Anthony please email Anthony.Faiella@AGinvestCanada.com

This information does not constitute financial or other professional advice and is general in nature. It does not take into account your specific circumstances and should not be acted on without full understanding of your current situation and future goals and objectives by a fully qualified financial advisor.